Decoding Q1 2025 Infrastructure SaaS Investment Trends

In an era defined by macroeconomic uncertainty, the infrastructure software-as-a-service (SaaS) segment continues to demonstrate remarkable resilience. According to PitchBook's Q1 2025 Infrastructure SaaS VC Trends report, the first quarter of 2025 showcased both stability and strategic adaptation in this critical sector, revealing important signals for financial institutions, technology investors, and corporate strategists alike.

Beyond the Megadeal Effect: Sustained Capital Deployment

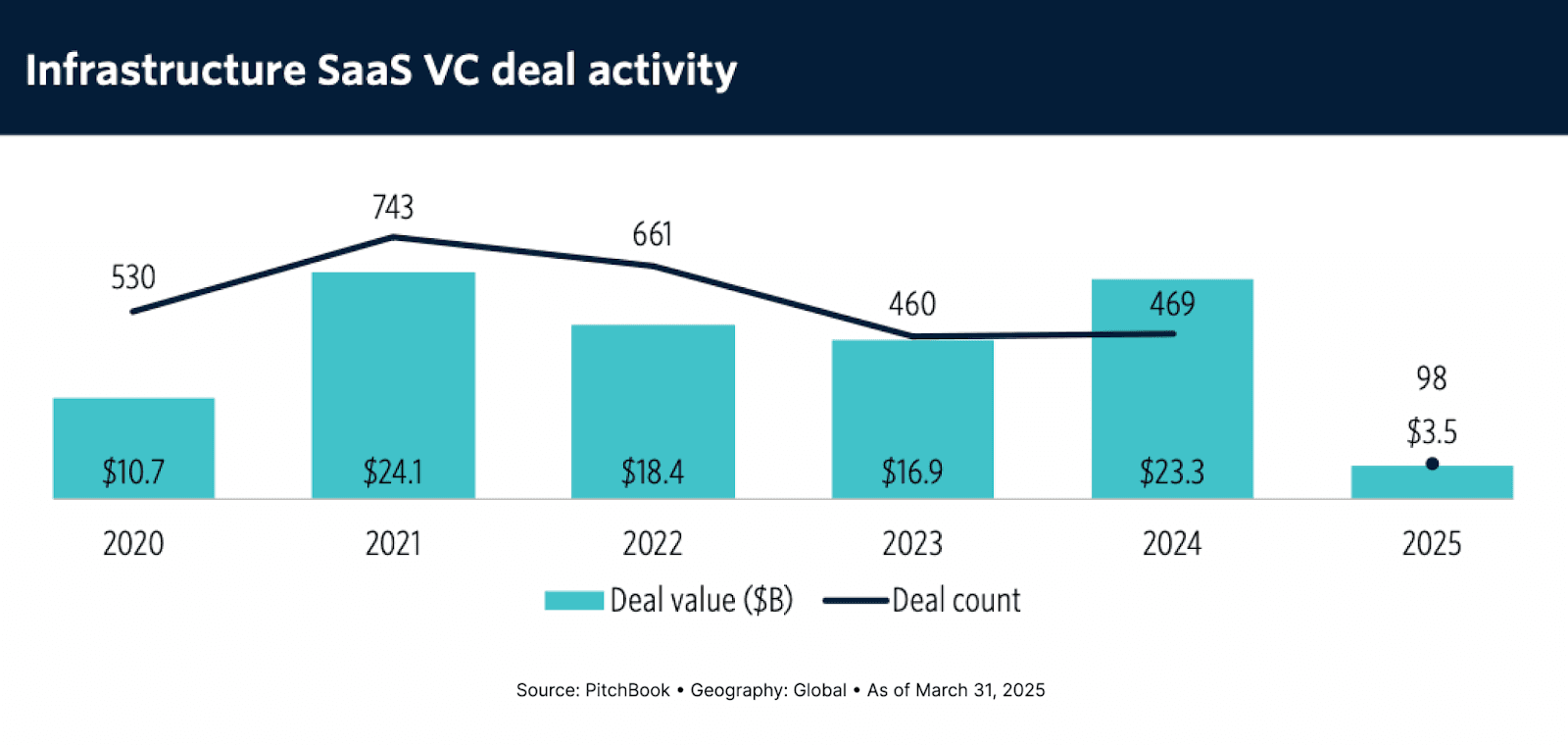

Q1 2025 marked a return to earth for infrastructure SaaS investment volumes following Databricks' massive $10 billion Series J in Q4 2024. Yet even without headline-grabbing megadeals, the sector maintained robust momentum with $3.5 billion deployed across 98 deals – representing a 23.1% increase in capital deployment when excluding the Databricks anomaly.

This sustained capital flow amid broader market caution signals institutional confidence in infrastructure SaaS as a foundational component of digital transformation. While deal count continued its gradual decline, dipping below triple digits for the first time, average deal sizes are increasing – suggesting greater investor selectivity and concentration on businesses with demonstrable product-market fit and clear paths to profitability.

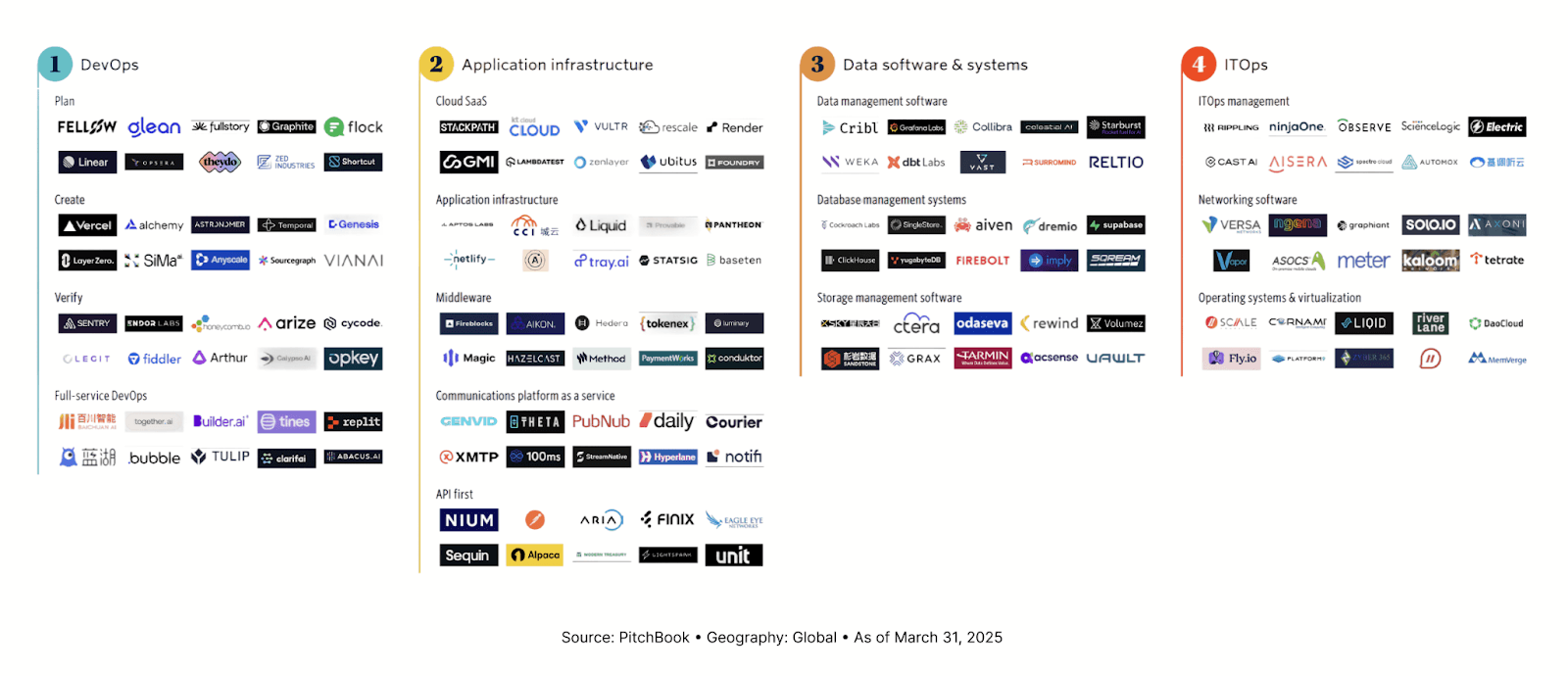

Segment Dynamics: AI-Driven Priorities Emerge

The quarter revealed notable shifts in investor priorities across infrastructure SaaS segments:

DevOps Resurgence: After a relatively quiet Q4, DevOps funding surged 280.4% quarter-over-quarter to $1.16 billion across 29 deals, narrowly claiming the top position by deal value. This reflects growing recognition that AI-enabled development operations represent a critical competitive advantage as organizations race to implement generative AI capabilities.

Data Software & Systems Consistency: This segment maintained strong momentum with $1.11 billion invested across 26 deals (up 42.4% QoQ excluding Databricks), highlighting the foundational importance of data infrastructure in the AI era. Companies like Celestial AI ($250M, $2.5B valuation) and Supabase ($200M, $2B valuation) exemplify the premium investors are placing on next-generation data management capabilities.

ITOps Strategic Concentration: Despite having the fewest deals (12), ITOps saw $746.3 million deployed – up 31.2% QoQ. NinjaOne's massive $500 million raise at a $5 billion valuation demonstrates how solution providers addressing critical IT management challenges can command substantial investment even in cautious markets.

Application Infrastructure Recalibration: This segment experienced the steepest decline (-64.4% QoQ) despite having the highest deal count (31), suggesting potential saturation and repricing in this mature category.

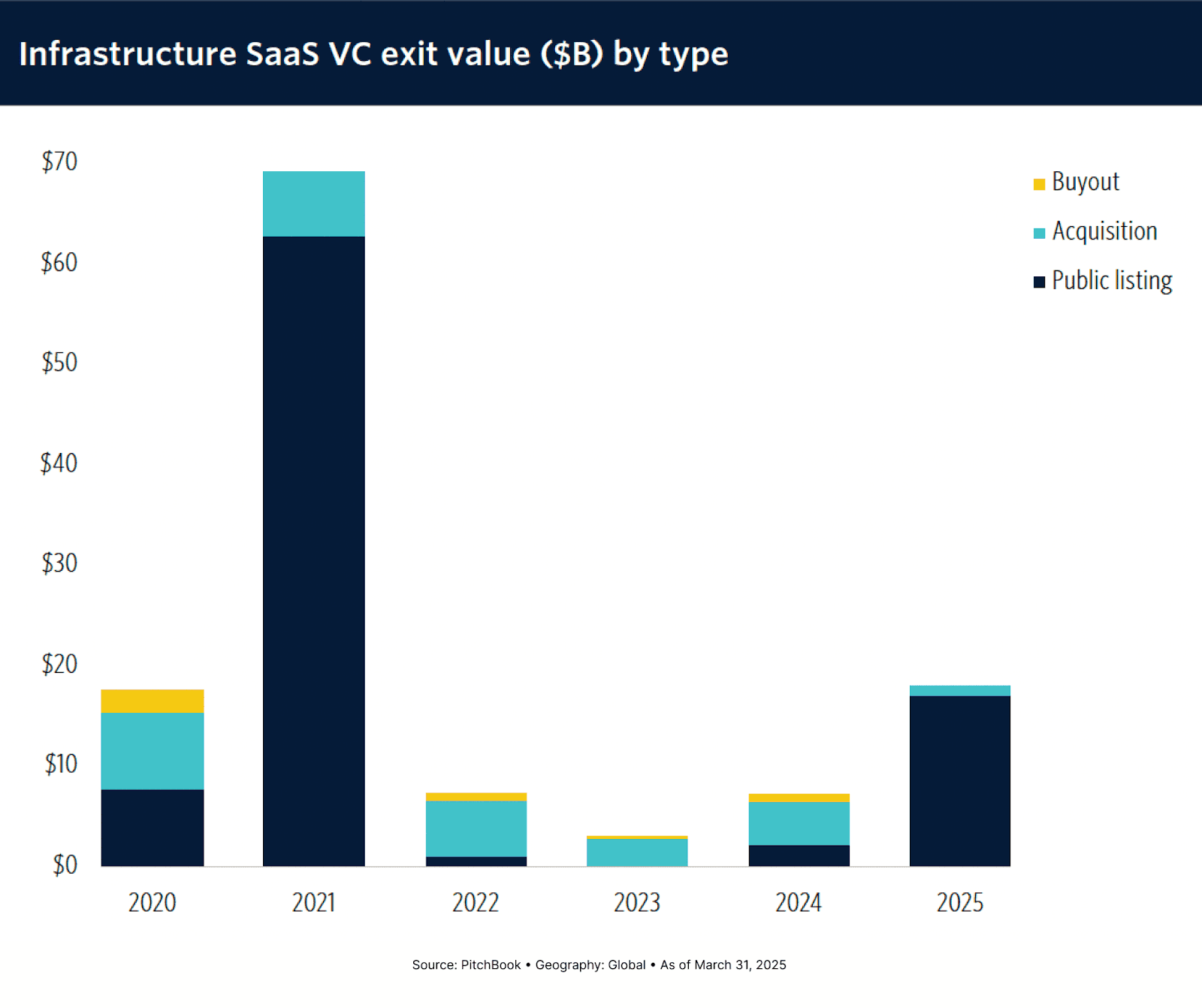

Exit Dynamics: CoreWeave Sets the Pace

Infrastructure SaaS exits roared back in Q1, with exit value jumping to $18 billion – the second-highest quarterly level on record. This was primarily driven by CoreWeave's landmark IPO, which valued the company at $17.1 billion.

CoreWeave's successful public debut carries particular significance. As a specialized cloud infrastructure provider optimized for AI workloads, its warm market reception validates the thesis that infrastructure optimized for AI-driven workflows represents a massive opportunity. The company's explosive revenue growth – up 420% year-over-year to $981.6 million in Q1 – exemplifies the scale opportunity in AI-enabled infrastructure.

Beyond CoreWeave, strategic acquisitions dominated the exit landscape, with NVIDIA's purchase of Gretel ($320M) and NXP Semiconductors' acquisition of Kinara ($307M) highlighting the appetite for specialized infrastructure capabilities among established technology leaders.

The AI-Infrastructure Nexus: Core Market Thesis

The quarter's investment patterns reinforce a clear market thesis: AI is transforming infrastructure from a backend utility to a strategic differentiator.

This manifests across three key dimensions:

Data Infrastructure Primacy: The massive valuations commanded by data management startups – with Celestial AI, Supabase and Turing all securing rounds at $2+ billion valuations – reflects recognition that next-generation AI applications demand sophisticated data infrastructure.

Defensive Posture Enhancement: As AI capabilities proliferate, the attack surface for digital systems expands exponentially. This is driving significant investment in defensive infrastructure, with security, compliance, and resilience becoming non-negotiable requirements.

Development Velocity Imperative: Companies capable of accelerating AI-enabled software development (as evidenced by strong funding for DevOps providers) are capturing premium valuations as organizations race to integrate AI capabilities into their products and workflows.

Investment Implications: Strategic Considerations

For financial institutions and corporate strategists monitoring the infrastructure SaaS landscape, several strategic considerations emerge:

Valuation Discipline Amid Strategic Necessity: While total funding remains robust, the declining deal count suggests greater investor selectivity. The days of indiscriminate capital deployment are over, yet strategic infrastructure capabilities command significant premiums when demonstrating clear differentiation.

Vertical-Specific Infrastructure Opportunity: General-purpose infrastructure is giving way to specialized solutions optimized for specific workloads or industries. Particularly in regulated sectors like banking and healthcare, purpose-built infrastructure addressing unique compliance and operational requirements represents a significant opportunity.

Integration vs. Best-of-Breed Tension: The market is navigating the perpetual tension between integrated platforms and best-of-breed solutions. Strategic acquirers like IBM (8 deals since 2020) and NetApp (7 deals) are actively consolidating capabilities, yet specialized providers continue to secure significant funding.

Talent as Competitive Differentiator: The companies attracting premium valuations typically feature technical founding teams with deep domain expertise. In a market where technical talent remains constrained, this expertise commands significant value.

Looking Forward: Key Trends to Monitor

As we progress through 2025, several developments warrant particular attention:

Infrastructure-as-Code Evolution: The boundaries between infrastructure and application layers continue to blur as infrastructure becomes increasingly programmable. This trend is accelerating with AI-driven automation of infrastructure management.

Private-to-Public Value Translation: CoreWeave's successful IPO suggests public markets may be warming to infrastructure SaaS companies with clear AI alignments, potentially creating more exit opportunities for well-positioned startups.

Strategic Consolidation Acceleration: As AI capabilities become table stakes, strategic acquirers will likely accelerate their consolidation of specialized infrastructure providers, creating potential exit opportunities for early-stage companies with differentiated capabilities.

Regulatory Impact Assessment: Evolving regulatory frameworks around AI will create both challenges and opportunities for infrastructure providers, particularly those addressing data governance, sovereignty, and compliance requirements.

Resilient Foundation for Innovation

Despite macroeconomic headwinds, Q1 2025 demonstrates that infrastructure SaaS remains a resilient foundation for innovation and investment. The continued strong capital deployment – particularly in AI-aligned segments – reflects recognition that as digital systems become increasingly central to organizational value creation, the infrastructure enabling these systems represents a strategic priority worthy of substantial investment.

For financial institutions and corporate strategists, the infrastructure SaaS landscape offers both challenges and opportunities. Those capable of identifying specialized providers addressing emerging needs, particularly at the intersection of AI and traditional infrastructure, stand to benefit substantially as digital transformation accelerates across industries.

Related News